You are here

Beijing’s Lead in Renewable Energy: Why India Needs to Introspect?

Summary: The perception of renewables as the future source of energy is gradually gaining traction. Major powers including the US, UK, Australia, Japan and China are moving at a fast pace to enhance their renewable energy capacity. Amongst these powers, China has already emerged as a leading country in the renewable energy sector. Currently it leads the export of renewable energy technology and controls the supply chain of rare earth minerals considered crucial for renewable energy technology production. Although compared to China the Indian renewable energy industry is at a nascent stage, New Delhi is making huge strides in the sector in terms of investment and capacity building. Given meticulous planning and sustained investment, India can expand its renewable energy industry to the extent of addressing future global need for renewable energy. Against the backdrop of Chinese pre-eminence in the renewable energy industry, this issue brief explores the potential challenges and opportunities that lie ahead of India for emerging as a renewable energy superpower.

Introduction

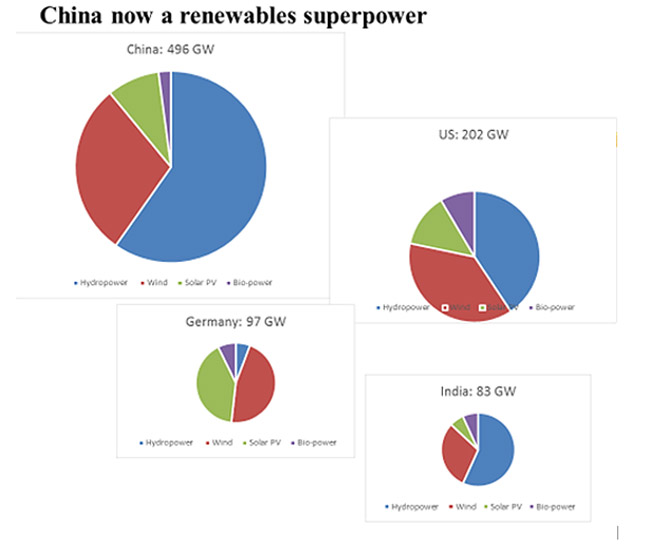

The potentially damaging impact of prolonged fossil fuel use on global climate has elevated renewable energy resources as the future global fuel. Moreover, falling cost of renewable energy production and increasing demand for clean power in the developing countries have added to the strategic value of the renewable industry.1 Accordingly, a number of countries including the US, UK, China, India, Australia and France are moving at a fast pace to master clean technology and export green energy. China, the world’s largest greenhouse gas emitter, has also emerged as one of the leading countries in the renewable energy sector.2 Over the years, China has expanded its domestic renewable energy power base3 and surpassed the West to become a leading exporter of renewable energy technology.4 Reportedly in 2020, China’s domestic renewable energy installation accounted for half of global installation that year.5 Also, China dominated the production and export of renewable energy technologies like wind turbines, crystalline silicon PV modules (used in solar cells), and lithium-ion battery cells (used for electric vehicles).6 It is noteworthy that with increasing tilt towards clean energy alternatives due to climate change concerns, its experiential and technological superiority in this space will likely accrue significant economic and geopolitical benefits to Beijing.

Compared to China, the Indian renewable industry is at the nascent stage. However, the country is investing aggressively in the sector as India aspires to achieve 175 GW of renewable capacity by 2022 and 523 GW by 2030.7 Currently, India stands at the fourth position globally for overall installed renewable energy capacity and is running the world’s largest renewable energy expansion programme.8 Also, recently the National Solar Energy Federation of India (NSEFI) has set up the Renewable Energy Export Promotion Council of India to promote Indian export of renewable energy.9 Therefore, as India’s strides in the renewable sector are increasingly gaining pace, it gives an opportunity to assess what potential challenges and opportunities arise for India in the face of China’s growing dominance in the climate industry.10

China’s Focus on Renewable Energy Industry

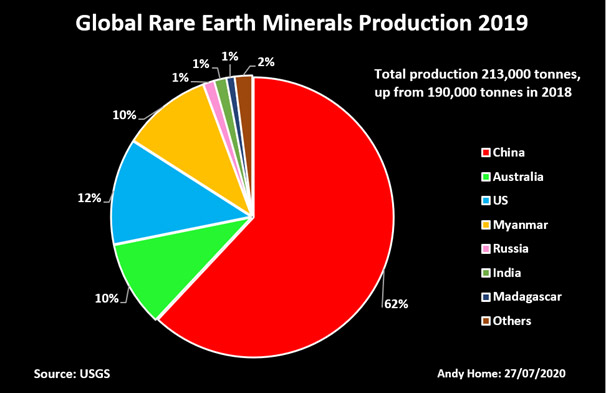

China wants to dominate the renewable energy sector due to its increasing strategic value as future energy resource. To that end, China’s endeavours in the renewable energy space have been threefold—acquisition of resources, gaining an edge in technology and dominating the market. For instance, despite harbouring the largest reservoir of rare earth minerals required to manufacture green energy components, China is still striving to purchase offshore mining rights to tighten its grip over the world’s resource base.11 Existing studies note that China holds more than a third of the world’s known reserves and is the third-largest miner of rare earth minerals. Nevertheless, Chinese companies are buying up lithium reserves in Chile12 and Argentina13 and have signed agreements with African countries like the Democratic Republic of Congo (DRC) and Zambia to mine copper and cobalt.14 Since rare earth minerals are termed as the oil of new age due to their critical manufacturing value for both defence equipment and green energy components, China is evidently aiming to secure sufficient resource to gain leverage in diplomatic bargaining in the future. Also, as China will be able to regulate the essential raw material supply chain15 , it could aid China to retain its leading position in the industry and influence future advancements in the sector.

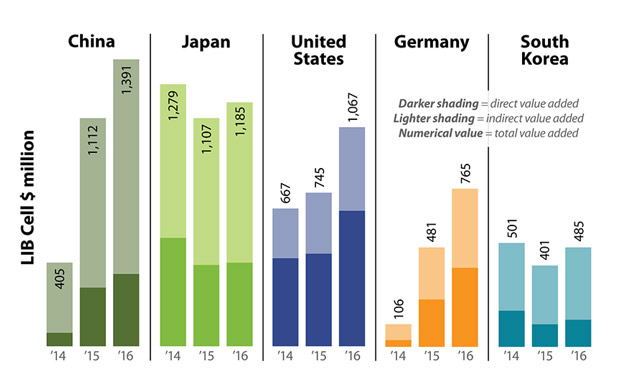

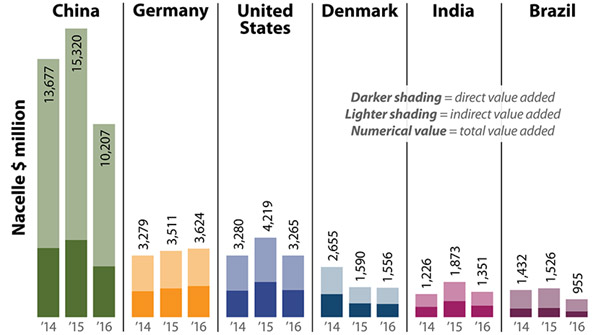

Wind Turbine Supply Chain Value Added, 2014–2016

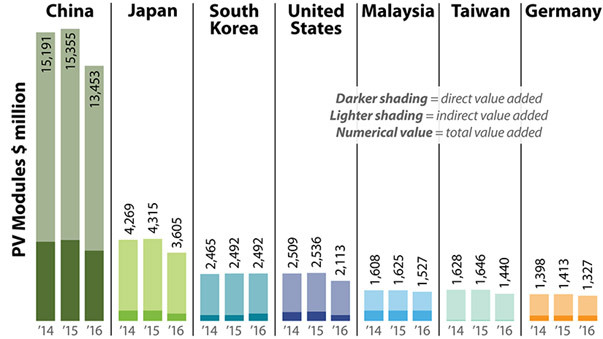

PV Module Supply Chain Value Added, 2014–2016

Vehicle Lithium-Ion Battery Cell Supply Chain Value Added, 2014–2016

The developmental trajectory of China’s renewable energy sector evinces a phased combination of foreign expertise and national investment and subsidies to incentivise technological advancement, which means that in the initial phase, Beijing drew heavily from the West to seed its renewable energy industry.16 However, after securing the initial framework from the West, a more economically confident China turned to developing its indigenous technological base by investing in its own companies and innovations. To elaborate on this further, it seems that when China was starting, in the 1990s, it received technology and investments for its renewable sector from Germany and later from OECD countries.17 These technology and capital transfers were instrumental in laying the foundation and expanding its renewable energy industry, especially in solar and wind power. Later, as China turned inward to self-reliance, technologies drawn from the West were amended, improved and given a Chinese label.18 Initiatives like Made in China 2025, channelled investments in research and development with emphasis on technological innovation in clean energy.19 Further, the Chinese government offered generous subsidies to shield domestic companies from foreign competition. Consequently, Chinese companies like State Grid, CATL, BYD and Three Gorges Renewables now lead in smart grids, smart meters, battery storage facilities, electrical vehicles, hydropower development among others. Furthermore, to limit competition in future innovation and preserve global dependence on China, Beijing aggressively patented these key technologies and now holds most of the renewable energy patents.20

Beijing strategised to dominate the clean energy market on the trade front by entrenching itself deeply within the global supply chain—from raw materials to finished consumer products.21 According to existing studies, China mines almost all of the world’s rare earth minerals used in electric motors and wind vehicles, which places it in a significant position in the manufacturing process.22 Also, it commands the renewable energy product market by being the world’s largest producer, exporter and installer of solar panels, wind turbines, smart grids, batteries and electric vehicles.23 China’s market dominance can be partly attributed to the rich endowments in rare earth minerals. However, a range of other factors were used by Chinese policymakers simultaneously; availability of cheap labour and venture capital, large domestic market and quick allocation of financial resources were used to drive down the cost of production, resulting in Chinese dominance of global markets.

It is noteworthy that China is also pushing for global recognition of its leadership status to expand its renewable energy market. As an exercise in that direction, Beijing is attempting to project its domestic environmental principle of ‘ecological civilisation’ as future recourse to sustainable development. For instance, President Xi in his address at the 15th Conference of the Parties to the Convention on Biological Diversity (COP 15) summit claimed ecological civilisation to be representative of development trend of human civilisation.24 Further, in a move to urge the global community to embrace this philosophy, Xi at COP 15 declared 1.5 billion yuan to support biodiversity protection in developing countries and post Summit a state bi-monthly magazine Qiushi emphatically declared China to be capable of advancing and constructing global ‘ecological civilisation’.25 Now, considering China’s ambitions of dominating the global renewable industry, the attempts to establish its philosophy as a guiding principle reveals the Chinese stratagem of opening markets for Chinese green technologies.26 That is by spurring countries to adopt a Chinese version of environmentalism, it is forcefully advocating the success of its climate policies and innovation that can be replicated in other countries by using Chinese technological solutions. As an experiment in this direction, Beijing, under the pretext of greening the Belt and Road Initiative (BRI), has started exporting various green technologies like smart electrical power grids, solar power panels, electric vehicles to BRI partner countries in Southeast Asia, Africa and Latin America.27

Furthermore, at the recent Conference of Parties 15 (COP 15) held in Kunming, China sharpened its rhetoric of mobilising more significant resources from finance, technology and capacity building for promoting ecological civilisation in developing countries.28 In future, it remains to be seen how this mobilisation facilitates the predominance of Chinese green technology companies.

China’s extensive control of the global renewable energy supply chain has sparked severe concerns in various countries. For example, speculations are rife in the US and EU about Chinese intentions of using export restrictions in rare earth minerals as leverage in bilateral disputes.29 On the other hand, in Asia, China-installed power grids have come under scrutiny over the security risks of Chinese control of the regional power supply.30 Last year, the Trump administration also moved an executive order to remove Chinese equipment from America’s electrical grid systems, citing security concerns.31 Driven by potential risks of Chinese control of the global supply value chain, major powers like the US, UK, EU, Japan and Australia have instituted several policy measures. These countries are striving to resist Chinese hegemonic practices, ranging from restrictions on technology transfer to China, increasing funding for R&D in renewable energy technology to forming partnerships for resource exploration and clean energy infrastructure.

Potential Challenges for India

For India, which shares a disputed border and strained bilateral ties with China, the challenges from Chinese dominance in the renewable energy sector are many. To begin with, Chinese monopoly over Rare Earth Elements (REE) supply puts India in a vulnerable spot. Due to both low domestic production and lack of cheap alternative supplies, Indian industries like automobile, defence, solar panel and wind turbine manufacturing are heavily reliant on Chinese rare earth mineral supplies.32 Chinese policymakers aware of the dependence are inclined to exploit the Indian conditions for strategic and political gains against New Delhi. For instance, this year, amidst the Galwan Valley crisis, Chinese solar equipment manufacturers threatened twice to stop polysilicon supplies to Indian power developers, resulting in completion delays and cost increment of solar power projects in India.33 These instances are likely to happen again in future, when bilateral disputes emerge between the two countries.

Second, China incorporating green technologies into border defence endangers India’s military security. A renewable-powered Chinese military will be less vulnerable to fuel disruption and capable of sustaining longer operations. It is also noteworthy that one of the critical goals of Chinese military modernisation is enhancing self-sufficiency. As a step towards self-sufficiency, the PLA has already built a renewable energy power grid for a border defence company under Western Theatre Command, which oversees the border with India. Reportedly, this logistical boost which aims at providing an all-weather power supply to the troops, is expected to make them fully ready to fight a war at all times.34 Needless to say that this measure will not only strengthen Chinese military presence along the border, but will also provide a greater operational edge to execute surveillance and reconnaissance in border areas. Therefore, Indian border regions could be exposed to a greater Chinese threat in times to come.

China has become a key energy partner of various South Asian and Southeast Asian countries owing to trade and investment in renewable energy projects and infrastructure building. Since 2014, Chinese equity investments have financed 12,622 MW of solar and wind power projects in South and Southeast Asia.35 Further, several state-owned companies like Power Construction Corporation of China,36 State Grid Corporation of China, China Three Gorges Corporation, Huadian have a strong presence37 in the renewable energy infrastructure markets of Pakistan, Bangladesh, Malaysia, Vietnam, Indonesia and Laos. Additionally, China is also planning to construct a continent-wide renewable energy Global Energy Interconnection (GEI) supported by Chinese technology and infrastructure.38 Given both the regions’ significance to Indian global aspirations, this increasing energy interlinkage with China heightens New Delhi’s geopolitical and economic challenges. Especially because Beijing aims to build a regional energy integration centred on China which will foster its political and economic influence,39 and leverage its extant dominant position, Beijing can influence tender allocation, consumer demand and technological standardisation to complicate Indian companies’ market access in these countries.

Opportunities for India

In contrast to China, India contributes only 7 per cent of the greenhouse gas emissions. Even so, and despite the considerable development gap with China, India has committed to achieving carbon neutrality by 2070, that is, within 10 years of China achieving the same.40 Further, in a significant step towards promoting and harnessing clean energy, India, in six years, launched two high-level initiatives—the International Solar Alliance (ISA) with France in 201541 and the One Sun One World One Grid–Green Grids Initiative (OSOWOG-GGI) with the UK in 2021.42 Furthermore, at the 2021 Leaders’ Summit on Climate, India demonstrating its responsibility to meet the Paris Agreement goals, collaborated with Washington to launch the US–India Climate and Clean Energy Agenda 2030 Partnership.43

Therefore, in light of these positive initiatives, New Delhi is being viewed as a leader and key partner in the climate industry by the international community.44 Countries reasonably concerned about China’s attempts to gain an unfair advantage over others in the renewable energy industry have reached out to New Delhi to strengthen their counter-balancing efforts.45 The British Company Ernst & Young identified India’s renewable energy market as the third most attractive destination for investment opportunities.46 Accordingly, UK and EU have evinced considerable interest in green energy technological transfers and financing green projects to strengthen India’s clean energy infrastructure.47 More importantly, the US is keen to deepen clean energy cooperation with India. For instance, the US restricted to China, transfer of semiconductor technology required in clean energy equipment.48 However, it forged technical collaboration with India on the same under the QUAD alliance.49 Besides, to boost US–India clean energy ties, Washington DC is even deliberating the passage of ‘The Prioritizing Clean Energy and Climate Cooperation with India Act of 2021’.50

If passed, the proposed legislation will deepen US involvement in India’s renewable energy sector. Similarly, towards the East Asian and Southeast Asia, countries eager to cut down reliance on China and diversify energy import options have partnered with India. For example, Japan’s International Cooperation Agency (JICA) lent around 4,400 crores to Indian banks and financial institutions over a period of 10 years to create renewable energy capacity.51 Taiwan, on the other hand, is in talks with India over building a chip manufacturing plant that would supply electric vehicles to India, and India–ASEAN countries are actively discussing ways to complement each other’s renewable energy policies and mutually address the energy needs.52

These recent developments offer considerable opportunities for India to expand its renewable energy sector. It already ranks as the fifth largest producer of renewable energy. Consequently, the financial support from the US, UK, EU and Japan will enable India to enhance its power generation capacity by developing critical areas like clean energy technology innovation, improving countrywide grid connectivity, transmission and energy storage capacity. Moreover, with multilateral initiatives like ISA and OSWOG-GGI, it will be easier for New Delhi to cut through the emerging China-centred regional energy integration and build a global energy congregation including trade partners from Asia, Africa and Europe.

Another potential area of cooperation is rare-earth mineral exploration. Reportedly, New Delhi and other QUAD members are contemplating building a rare-earth procurement supply chain to counter China’s dominance in supply of these crucial minerals.53 It is noteworthy that India currently holds 6 per cent of known rare-earth mineral reserves but accounts for only 1 per cent of rare-earth mineral production.54 Therefore, such collaboration, if materialised, will be a major positive outcome for India as technology transfer relating to rare earth mineral refining will allow India to utilise its own resources and reduce dependence on China efficiently. Simultaneously, India’s leadership status in renewable energy production can be utilised by New Delhi to join efforts to create a more level playing field for green technology companies.

As the global renewable energy industry is slowly taking shape, India’s leadership and diplomatic clout can be directed towards drafting laws for technological standardisation. This in turn, will effectively secure market access and protect against arbitrary imposition of technical standards. Lastly, with more advancements in green technology, India can extend civilian partnerships to explore military usage of renewable energy. In that context, India using the QUAD platform can promote joint harnessing of solar and ocean energy to fuel naval operations in the high seas. In addition, further joint military exercises using solar and wind energy to support combat operations can be held with South Asian and Southeast Asian countries.

In conclusion, it can be said that due to intensifying calls for energy transition towards renewables, the green energy sector is likely to become an arena of more intense competition. China’s dominance in the renewable energy industry is a grave reality. Accordingly, New Delhi will have to evaluate its strengths and chalk out a careful strategy to manage the increasing renewable energy competition.

Views expressed are of the author and do not necessarily reflect the views of the Manohar Parrikar IDSA or of the Government of India.

- 1. David Frankel, Nadine Janecke, Florian Kühn, Ingmar Ritzenhofen and Raffael Winter, “Rethinking the Renewable Strategy for an Age of Global Competition”, McKinsey&Company, 11 October 2021.

- 2. “Report: China Emissions Exceed all Developed Nations Combined”, BBC, 7 May 2021.

- 3. Verity Ratcliffe, “China, U.S. Made 2020 a Record Year for Renewable Power Growth”, Bloomberg Green, 5 April 2021.

- 4. Charlie Campbell, “China is Bankrolling Green Energy Projects Around the World”, Time, 1 November 2019.

- 5. “China Boosts Renewable Energy Results in 2020”, International Electrotechnical Commission, 18 June 2021.

- 6. “A New World: The Geopolitics of the Energy Transformation”, IRENA, 2019.

- 7. “India on Track to Achieve 450 GW Renewable Energy Target by 2030: Power Minister”, Mint, 14 August 2021.

- 8. “Summary”, Renewable Energy, Make in India.

- 9. “India Need to Focus on Export of Renewable Energy: Pranav Mehta, Chairman, NSEFI”, ET Energy World, 19 June 2020.

- 10. Roderick Kefferpütz, “Green Deal Reloaded - Why the European Climate Policy Won’t Happen Without China”, Institut Montaigne, 28 April 2021.

- 11. Mary Hui, “A Chinese Rare Earths Giant is Building International Alliances Worldwide”, Quartz, 19 February 2021.

- 12. Francois Austin, “The Future of Energy is Being Shaped in Asia”, World Economic Forum, 27 December 2019.

- 13. Kenji Kawase, “Chinese Investors Jostle Over Argentine Lithium Mines”, Nikkei Asia, 13 October 2021.

- 14. Magnus Ericsson, Olof Löf and Anton Löf, “Chinese Control over African and Global Mining—Past, Present and Future”, Mineral Economics, Vol. 33, 2020, pp.153–181.

- 15. Leslie Hook and Henry Sanderson, “How the Race for Renewable Energy is Reshaping Global Politics”, Financial Times, 4 February 2021.

- 16. Scott Malcomson, “How China Became the World’s Leader in Green Energy”, Foreign Affairs, 28 February 2020.

- 17. Frauke Urban, “China's Rise: Challenging the North-South Technology Transfer Paradigm for Climate Change Mitigation and Low Carbon Energy”, Energy Policy, Vol. 113, February 2018, pp. 320–330.

- 18. Ibid.

- 19. Melissa Cyrill, “What is Made in China 2025 and Why Has it Made the World So Nervous?”, China Briefing, 28 December 2018.

- 20. No. 6.

- 21. Francis Gassert, “China Dominates the Clean Energy Supply Chain”, New America, 3 March 2020.

- 22. No. 15.

- 23. No. 6.

- 24. “Eco-civilization Illuminates Path to Sustainable Future”, Xinhua, 14 October 2021.

- 25. Ibid.; He Yin, “China Determined to Pursue Green Development and Build Shared Future for Humanity and Nature”, Qiushi, 13 October 2021.

- 26. Sarah Ladislaw and Nikos Tsafos, “Beijing is Winning the Clean Energy Race”, Foreign Policy, 2 October 2020.

- 27. Kelly Sims Gallagher and Qi Qi, “Climate Proofing China’s Belt and Road Initiative (BRI)”, Climate Policy Lab, The Fletcher School, Tufts University, 7 May 2021.

- 28. Hou Liqiang and Yang Wanli, “COP 15 Places Eco-civilization Under Spotlight”, China Daily, 12 October 2021.

- 29. Jason Rogers, “'Don’t Say I Didn’t Warn You': China Gears Up to Weaponize Rare Earths Dominance in Trade”, Bloomberg,29 May 2019; “Questions about China's Rare Earths Export Restrictions”, European Parliament, 7 May 2021.

- 30. Akane Okutsu, Cliff Venzon and Ck Tan Nikkei staff writers, “China's Belt and Road Power Grids Keep Security Critics Awake”, Nikkei Asia, 3 March 2020.

- 31. Adam Xu, “US Moves to Pull Chinese Equipment From Its Power Grid”, Voice of America, 9 May 2020.

- 32. Shebonti Ray Dadwal, “China’s Continuing Rare Earth Dominance”, MP-IDSA Comment, 27 September 2019.

- 33. Shashwat Mohanty, “A War Over Rooftop Solar Panels is Brewing between Indian and Chinese Firms”, Economic Times, 28 July 2021.

- 34. Liu Xuanzun, “PLA Builds Renewable Power Grids for Border Defense Outposts in Plateau, Islands”, Global Times, 21 January 2018.

- 35. No. 4.

- 36. Tyler Roney, “What are the Impacts of Dams on the Mekong River?”, The Third Pole, 1 July 2021.

- 37. Tim Buckley and Simon Nicholas, “China’s Global Renewable Energy Expansion”, Institute for Energy Economics and Financial Analysis, January 2017.

- 38. Phillip Cornell, “International Grid Integration: Efficiencies, Vulnerabilities, and Strategic Implications in Asia”, Atlantic Council, 9 January 2020.

- 39. Phillip Cornell, “Energy Governance and China’s Bid for Global Grid Integration”, Atlantic Council, 30 May 2019.

- 40. Chetan Chauhan, “Explained: PM Narendra Modi’s Commitments at COP26 Summit on Climate Change”, Hindustan Times, 3 November 2021.

- 41. “International Solar Alliance (ISA)”, Climate and Clean Air Coalition, 2019.

- 42. “One Sun, One World, One Grid: India-UK's Ambitious Global Solar Grid Plan Explained”, The Times of India, 3 November 2021.

- 43. “U.S.-India Joint Statement on Launching the ‘U.S.-India Climate and Clean Energy Agenda 2030 Partnership’”, Office of the Spokesperson, U.S. Department of State, 22 April 2021.

- 44. Sumant Sinha, “Why India is the New Hotspot for Renewable Energy Investors”, World Economic Forum, 14 January 2020.

- 45. “World Wants India as Counter-balance to China Amid Global Economic Woes: SpiceJet's Singh”, PTI, 21 January 2019.

- 46. “India Retains 3rd Position in RE Investment Attractiveness Index”, PTI, 13 October 2021.

- 47. “COP26: UK Launches India Green Guarantee, Commits New Funds for EVs in India”, PTI, 1 November 2021; Souvik Bhattacharjya, “The EU ‘Green Deal’: An Opportunity to Strengthen EU-India Relationship”, KAS-MDPD, 18 June 2021.

- 48. Karen Freifeld, “U.S. Imposes New Rules on Exports to China to Keep Them from Its Military”, Reuters, 27 April 2020.

- 49. Raghu Krishnan, “Quad Alliance Joins Hands to Secure Semiconductor, 5G Tech Supply Chains”, Economic Times, 26 September 2021.

- 50. “US Senator Introduces Legislation to Boost India-US Ties in Clean Energy”, PTI, 14 September 2021.

- 51. Pia Krishnakutty, “Lent Indian Banks Rs 4,400 cr Over 10 Years for Renewable Energy Work, JICA India Head Says”, The Print, 4 November 2021.

- 52. “India has China on its Toes as Modi Govt Engages Taiwan to Solve Domestic Chip Shortage”, Bloomberg, 27 September 2021; Prabir De and Durairaj Kumarasamy, “ASEAN-India Energy Cooperation:

Current Status and Future Scope of Cooperation”, AIC Working Paper, RIS, March 2020. - 53. “Quad Tightens Rare-earth Cooperation to Counter China”, Nikkei Asia, 11 March 2021.

- 54. Ibid.